Companies that deliver clear aligner treatment to customers’ homes are changing the way people transform their smiles. Historically, the only way to adjust your teeth was to see a dentist or orthodontist for braces or Invisalign. Today, home clear aligner products like SnapCorrect are designed to make getting the smile you want affordable and convenient.

SnapCorrect was one of the first home aligner companies to hit the US market, and with some of the lowest prices in the industry, they’re certainly worth considering. Read on to find out if SnapCorrect is the right fit for your smile goals.

Table of Contents

What is SnapCorrect?

Based out of Vancouver, Washington, SnapCorrect is an online company that’s designed to offer convenient and affordable teeth aligner products that let you transform your smile from home. SnapCorrect’s clear aligners look and feel similar to Invisalign — they’re designed to fit the contours of your teeth, moving them without a single metal bracket. However, unlike Invisalign, treatment doesn’t require any trips to the dentist. Instead, after they approve you for treatment, one of SnapCorrect’s dental professionals will develop your plan. The company will then ship the clear aligners straight to your doorstep for home application.

If you’re saying “sign me up,” you should know that SnapCorrect is just one of several online companies to offer home-based clear aligner treatment. With the recent rise in home aligner popularity, there are now multiple competitors providing a very similar service, including Byte, SmileDirectClub, NewSmile, and AlignerCo. Most of these companies are relatively young. In fact, SnapCorrect started in 2017 and it’s one of the older companies in the home aligner industry.

SnapCorrect aims to stand out by offering free teeth whitening for life plus an affordable price.

Like other home-based clear aligner products, SnapCorrect is primarily a cosmetic treatment and only designed to correct mild-to-moderate cases of spacing and crowding, along with mild bite issues. They won’t automatically disqualify you from treatment if you have a more severe case or a jaw misalignment like overbite or underbite, but you’ll likely see better results from a treatment plan that is managed in-person by a dental professional, such as braces or Invisalign.

How Does SnapCorrect Work?

To ensure that SnapCorrect can provide the results you’re after, their team will first need to look at your smile. Get started by ordering an impression kit from their website, which you’ll use to make molds of your top and bottom dental arches. After you submit these molds, SnapCorrect’s licensed dental professionals will use them to determine if you’re a good candidate for treatment.

If so, they will begin work on your custom aligners and treatment plan. They’ll also send you a treatment preview and Consent to Treat form, which you’ll sign to get started. At this point, the company will produce your clear aligners and ship them by mail. Diligently wear your aligners for around 22 hours each day and your teeth will gradually shift over the next 3–9 months (on average).

Unboxing Impression Kit

Unboxing Impression Kit Creating Smile Impressions

Creating Smile Impressions Mailing Back Impressions

Mailing Back Impressions

Is SnapCorrect Legit? We Think So!

Although they didn’t make our list of the top five at-home aligner companies, we think SnapCorrect’s low price point makes them a worthwhile option for anyone who’s comfortable working with a smaller company.

SnapCorrect vs. Byte (Our #1 Recommendation)

SnapCorrect is definitely cost-effective, but if you’re looking to get the most bang for your buck, in our opinion, Byte is tough to beat. Your perfect match for orthodontic treatment will depend largely on your personal priorities, your budget, and your dental condition. That said, se think Byte is an excellent treatment option for most people with mild-to-moderate cases of misalignment.

For a closer look at some of our other top picks, check out our in-depth comparison of the five best home-based clear aligners below.

Pros & Cons of SnapCorrect

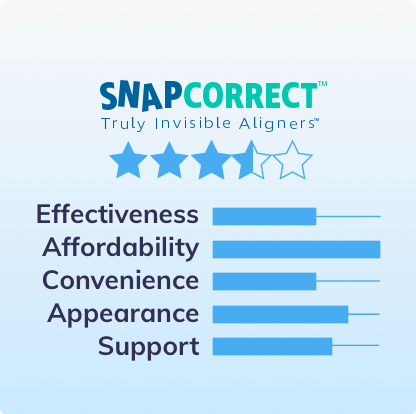

SnapCorrect didn’t make the list of our top five at-home aligner treatments, but that doesn’t mean they’re a bad option. It just means that we think there are a couple of areas where they could grow and where other companies provide more attractive perks. We based our rankings on a comparison of five criteria: scope of treatment, affordability, convenience, appearance, and customer experience.

Further down, you’ll find a lot more detail on how SnapCorrect stacks up category by category, but here’s a quick summary of the biggest pros and cons:

SnapCorrect Pros

- At $1,749, SnapCorrect is more affordable than many competitors, especially in-person treatments like Invisalign.

- They include your first set of retainers in your aligner package. Other companies charge you $80–125 at the end of treatment for retainers.

- SnapCorrect offers free teeth whitening for life once you are a customer. Some competitors include free whitening, but only a few months worth.

- SnapCorrect crafts their aligners with plastic from Raintree Essix, one of the largest dental equipment and dental material suppliers in the US This suggests these aligners are of reasonably high quality.

- Aligners are marketed as clearer and less visible than those offered by competitors. However, in our opinion, the difference in visibility is not meaningful. Some customers may actually dislike the shinier plastic used in these aligners.

SnapCorrect Cons

- SnapCorrect does not currently offer retail locations where you can get your teeth scanned instead of completing an impression kit. You’ll need to take dental impressions on your own.

- While some competitors offer nighttime-only plans that only require ten hours of daily wear, SnapCorrect only offers the standard, 22-hours-per-day option.

- SnapCorrect doesn’t provide any remote monitoring during treatment.

Our Review Methodology

Smile Prep’s reviews are prepared and presented from the perspective of a well-informed consumer. Our starting point for all of our reviews is a careful survey of a company’s marketing claims and available third party customer reviews. We rely on the accuracy of company claims and do not independently verify them. Our reviews use this information to help our readers get information about the available options in a centralized location. You can learn more about our review process by checking out our publishing principles.

Scope of Treatment

SnapCorrect aims to deliver cost-effective teeth straightening that fits into the schedule of busy adults. But before you get your heart set on their aligners for your treatment, you have to know if they will meet your orthodontic needs. And the answer to that depends on if your case falls within their scope of treatment.

SnapCorrect was designed to make cosmetic alterations, not those with major effects on oral health.

Even small shifts can help your teeth stay cleaner, resulting in a healthier smile over time. SnapCorrect’s FAQ page says, “we can reduce gaps, reduce crowding, and straighten most teeth, but we cannot correct every case.”

That’s fairly vague, but here are the conditions at-home aligners can typically treat:

- Mild-to-Moderate Crowding: Where the teeth are too close together, sometimes even overlapping each other.

- Mild-to-Moderate Spacing: When the teeth are too far apart, often causing crowding in other teeth. Mild-to-moderate gaps are typically 3mm wide or less.

- Mild-to-Moderate Overbite or Overjet: When the upper front teeth extend too far over the lower ones (overbite) or protrude outward (overjet). In mild-to-moderate cases, this should be purely dental — not involving the jawbone.

- Limited Underbite: When the lower front teeth overlap the upper front teeth. In limited cases, it only involves certain pairs of teeth.

- Localized Crossbite: When some upper teeth sit inside the lower teeth. Typically, clear aligners work better with crossbites that affect the front teeth (anterior) than ones that affect the back teeth (posterior).

Most at-home aligner companies focus on what are called the “social six” — the frontmost six teeth in either arch. These teeth have the least complex roots, making them easier to move. This is where SnapCorrect focuses its treatment, though it can occasionally move other teeth. If they feel they cannot make the shifts you need, they will decline your case.

This scope of treatment is standard for remote care. However, it is more limited than in-office aligners, which can often address complex issues, such as overbite or underbite. Even express systems offered by dentists and orthodontists can exceed this scope of treatment, since they can incorporate attachments. So if speed is your top concern, your misalignment is complex, and you don’t mind office visits, Six Month Smiles or Invisalign Express might also be good options.

The big question, of course, is whether SnapCorrect can help you achieve your specific smile goals.

No matter how much time you invest in researching clear aligner options, digging into client testimonials, and comparing your teeth to those in before photos, you won’t know if any work for you until you get your teeth assessed. For SnapCorrect, this means completing an impression kit.

Once you complete yours, just ship it off and their team will review it. If you qualify for treatment, they’ll walk you through the next steps. If you don’t, you’ll likely need to go with an in-office aligner option.

A dental professional will design your aligner treatment.

The skill and experience of the person in charge of your care can significantly affect your treatment’s outcome. In a worst-case scenario, treatment at the hands of an inexperienced professional could even leave you with an annoying bite issue that you need to fix down the road.

On their FAQ webpage, SnapCorrect explains that dental technicians (individuals trained to use special software) are involved with analyzing your impression kit, approving you for treatment, and preparing your treatment plan. While the company is legally required to work with dentists at some level, it is unclear if the dentists they employ are working hands-on to develop treatment plans, or simply approve the plans developed by technicians.

SnapCorrect makes their aligners with plastic from Essix, a large and reputable company.

Most at-home aligner companies outsource their aligner production to large well-respected third-party manufacturers. For instance, SmileDirectClub used to work directly with Align Technology, the makers of Invisalign, and Byte has the backing of the widely respected Dentsply Sirona. SnapCorrect uses materials from Raintree Essix — who is also owned by Dentsply Sirona — so you can trust that their aligners contain high-quality plastics.

Affordability

Let’s face it: teeth straightening treatment isn’t cheap. The high price tag for braces and Invisalign has historically made transforming your smile a substantial financial burden. Making matters worse, health insurers seldom cover this type of cosmetic treatment, and dental insurance will typically reimburse just a small fraction of the cost.

This is where SnapCorrect’s low upfront price shines. All home aligner treatments are usually much more affordable than in-office options like Invisalign, which can cost $3,000 or more. And SnapCorrect is even less of a financial burden, making their treatment more accessible to a wide range of potential customers.

SnapCorrect’s $1,749 sticker price includes everything you need, and although it’s not the lowest price in the industry, we think it’s relatively affordable.

This sticker price is higher than AlignerCo and NewSmile, but lower than Byte and SmileDirectClub, and far less than Invisalign or other in-office aligners. It covers the cost of your impression kit, treatment plan, clear aligners, and teeth whitening. SnapCorrect also includes your first set of retainers with the purchase price, which will save you some money at the end of your treatment.

Other services like SmileDirectClub do not include retainers in the initial price, instead selling them at the end of treatment for around $100. It’s nice to know that, after your initial payment, SnapCorrect won’t spring any hidden costs.

SnapCorrect offers a payment plan option, but it requires a credit check and some may not qualify.

Even though SnapCorrect is much cheaper than braces or Invisalign, not everyone has $1,749 stashed in their junk drawer or under their bed. To make treatment more accessible, they offer financing through a third-party called Affirm. This is a great option if you can’t (or don’t want to) pay for a large lump sum at once. The only drawback is that Affirm requires a soft credit check, so not everyone will qualify.

By comparison, some of SnapCorrect’s competitors offer more flexible financing options, including ones that don’t require credit checks. Byte, AlignerCo, and SmileDirectClub each have in-house options that offer no-questions-asked financing to all customers, regardless of credit score.

Convenience

Aside from the cost, one of the biggest barriers to pursuing a more comfortable smile is traditional orthodontics’ substantial time commitment. Between work, family, social engagements, and personal time, your schedule is probably packed full, and scheduling dentist appointments every month would be a hassle. After all, it’s not exactly a trip to the beach. Nevermind taking time off work every month to attend your appointments.

In our view, home aligner companies like SnapCorrect make this kind of treatment much more convenient by shipping aligners to your home, no office visits necessary. Additionally, because most home aligners (SnapCorrect included) only treat milder misalignments, you can usually complete treatment in about half a year or less.

We think SnapCorrect is unquestionably more convenient than Invisalign or braces, but compared to its home aligner competitors, it’s about average.

SnapCorrect offers fewer startup options than other leading brands.

It might seem like the hardest part of home aligners is the treatment itself, but many customers actually find that getting started is more difficult.

Before developing your treatment plan and crafting your aligners, a home aligner company needs to get a look at your teeth. This is both to determine if you’re a suitable candidate and to create your treatment plan. All home aligner companies, including SnapCorrect, offer a kit that you can use to make molds of your teeth called an impression. You’ll mix together two different types of putty and place the mixture in a tray, then bite down on it to create a mold. When you’re done, you’ll mail this mold to your provider for review.

Most people don’t have any experience taking impressions of their teeth, so this process can be surprisingly difficult. But SnapCorrect thought ahead, so they’ll send you two sets of putty and trays, two chances to make a good impression of both your top and bottom arches.

Some of SnapCorrect’s competitors, however, go a step further, offering free 3D teeth scans at retail locations as an alternative to snail mail impression kits. SmileDirectClub, for example, has 100+ physical locations and 1,000+ partnering dental offices where a dental professional will take teeth scans for you. SnapCorrect doesn’t currently offer this option, but their customer support is always available to walk you through the impression kit process or offer much-needed encouragement.

Expect to wait around 5–6 weeks total before you start treatment.

You’ll need to exercise some patience after submitting your impression kit. Assuming you complete and submit it ASAP, you can expect to receive your treatment plan within 2–3 weeks. Once you approve your plan and sign SnapCorrect’s Consent to Treat form, it takes 2–4 additional weeks to manufacture and ship your clear aligners. So, you’ll need to wait a total of 5–6 weeks before your aligners show up on your doorstep, which is slightly longer than some of SnapCorrect’s competitors.

SnapCorrect treatment takes around 3–9 months on average.

Maybe your wedding is in five months. Or maybe you simply can’t wait to see your transformed smile. Whatever your timeline, it’s important to consider each provider’s average treatment times. Of course, it ultimately depends on the severity of your misalignment, but choose SnapCorrect and they say you can expect an average timeframe of around 3–9 months — pretty standard for at-home aligner treatments.

If you stumble upon SnapCorrect’s FAQ page, you’ll see that they claim some patients complete treatment in three months, but that some may take up to 18 months. These cases are most often outliers, but if you have a particularly complex case, it’s possible.

SnapCorrect includes teeth whitening for life, but they suggest holding off until you’ve finished your treatment.

Want to whiten your smile while you straighten your teeth? With most home aligners, you can. Every company we reviewed provides free whitening gel, and most allow you to use it at the same time as your aligners. You simply apply the gel or foam inside your aligners so that your teeth get brighter and straighter at the same time!

SnapCorrect, however, recommends finishing treatment first. They say that the whitening procedures might cause you to wear your aligners for less than the required 22 hours per day. Plus, they will send you special whitening trays after you complete treatment, and it’s better to have whitening trays that fit your finished smile.

On the bright side, SnapCorrect provides free whitening treatment for life, something no other company offers. So, even years after your teeth straightening treatment is complete, you can maintain your beautiful, dazzling white smile.

At the end of the day, we think SnapCorrect is a fairly low-hassle way to straighten your teeth — much easier than in-office clear aligner treatments. However, in our opinion, they haven’t created as streamlined a process as some competitors, especially for whitening and getting started.

Appearance

A large reason for clear aligners’ skyrocketing popularity among adults is their low profile compared to traditional braces. Many adults cringe at the thought of sporting metal brackets to a job interview or date, or even in everyday life. That’s why many adults find clear aligners appealing.

That said, not all clear aligners are created equal in terms of appearance. While they’re all made from transparent, BPA-free plastic, each brand looks slightly different due to variations in materials and manufacturing processes.

SnapCorrect makes their aligners from smooth, shiny plastic and trimmed to follow the gums.

These are fairly different from the frosted-appearing aligners that Candid, SmileDirectClub, or Invisalign make. They call their aligners “Truly Invisible” because of the transparent material they use. Initially, clear and shiny might seem better. But here’s the thing: your teeth are naturally porous (which is why they can absorb stains from coffee, red wine, etc.) and these pores give them a matte surface. This is why we think “frosted” aligners can actually look more natural than shiny ones, which might appear unnaturally reflective.

That said, some customers actually like the shininess — they feel like it makes their smiles gleam. The frosted vs. shiny debate is largely subjective and influenced by personal preference. So, the shinier plastic SnapCorrect uses shouldn’t necessarily deter you, but it’s something to consider while you make your decision.

SnapCorrect trims their aligners in a scalloped fashion to match your unique gum line, similar to Invisalign.

We think scalloped aligners are slightly less visible, but they also don’t exert as much force on your teeth. Invisalign handles this deficiency by allowing your dentist to place special attachments on the teeth that anchor your aligners in place, empowering them to shift teeth more effectively. Since home aligners like SnapCorrect don’t involve in-person visits, this is not possible, so they typically can’t treat severe misalignments.

At-home aligners that cover the gums may distribute their force better than scalloped ones, though they’re arguably less ideal in terms of appearance and comfort. For this reason, we can’t recommend SnapCorrect’s scalloped aligners over competitors offering aligners that cover the gums, even if they are less noticeable.

Like other clear aligners brands, you’ll want to take out your SnapCorrect aligners before eating & drinking to avoid stains.

All clear aligners are susceptible to stains from food and beverages — that’s why it’s important to remove them before eating or drinking anything other than plain, cool water. SnapCorrect aligners are reasonably resistant to staining, although we certainly wouldn’t recommend drinking coffee or red wine with your aligners in.

Customer Experience

Considering the expense of orthodontic treatment and how valuable your smile is, you’ll definitely want a provider that cares about you and your progress. It can be difficult for remote companies to compete with the hands-on care offered by in-person treatments, but we think SnapCorrect does an adequate job providing helpful support.

SnapCorrect support is responsive and they offer a standard refund policy.

Have a question or concern? Need to get in touch? SnapCorrect is available by phone, email and webchat on weekdays from 9am–5pm Pacific Time. We tested all three options and found them quite responsive. When we used their website’s webchat, we received a response in less than five minutes.

SnapCorrect’s refund policy is fairly standard, but doesn’t go as far as some other companies. If they determine you’re not a suitable candidate for treatment, they will refund the cost of your impression kit, so it’s totally risk-free to inquire. But once you sign your Consent to Treat form after viewing your treatment preview, they won’t issue any refunds. However, if you find that your treatment isn’t progressing as expected, SnapCorrect will work with you to get you back on track.

What are SnapCorrect Customers Saying?

When we review a company like SnapCorrect, we start by digging through reviews to understand common customer issues and concerns. Currently, SnapCorrect only has a handful of online reviews, and many seem to be sponsored by the company.

Even so, the genuine online customer reviews we found often reported satisfaction with the service and customer support. Some customers, however, have reportedly run into problems getting their impression kits approved. These customers sometimes had to redo their impressions up to three separate times — a bit of a hassle, and a problem that most other companies don’t have.

Invisalign vs. SnapCorrect

While we think SnapCorrect is a great clear aligner company, there are plenty of other options to consider, and the most widely known is Invisalign. Invisalign is a traditional in-office treatment option, so it requires multiple office visits, but can treat a wider scope of conditions.

If you have a severe condition, or you’d prefer face-to-face oversight, Invisalign could be a great fit. While home aligner companies like SnapCorrect are entirely remote, a dentist or orthodontist must administer Invisalign in person, and it requires office visits every 4–10 weeks on average.

This allows your dentist to incorporate elastics or Invisalign’s proprietary Smartforce attachments, which improve aligner retention and orthodontic tooth movement.

Of course, Invisalign’s in-person care and intensive clinical treatment come at a higher cost, often $3,000–$8,000, depending on your condition’s severity and your dentist’s rates. And it often takes longer too — usually 12–18 months compared to SnapCorrect’s 3–9 month average.

Whether you choose an in-office treatment like Invisalign or an at-home one like SnapCorrect largely depends on your unique condition and personal priorities. For details on Invisalign’s benefits, drawbacks, and procedures, take a look at our in-depth Invisalign review.

Byte vs. SnapCorrect

Byte is our #1-ranked clear aligner service thanks to their convenience, personalized customer service, and efficiency. They claim an average treatment plan length of just 4–5 months and give every customer a HyperByte device — which uses gentle micro-pulses that they say might help reduce discomfort.

Byte has a nighttime-only treatment plan (called Byte At-Night) that only requires ten hours of wear per day. They craft their nighttime aligners specifically for nighttime wear using a grind-resistant plastic, something no other company does.

We think Byte offers more personalized customer service than SnapCorrect too. They assign each patient a “Byte Advisor” who serves as your contact for any questions or concerns at the beginning of your treatment. Additionally, their Byte-for-Life Guarantee keeps your smile in place for life, providing refinements if your teeth ever shift down the road, as long as you’ve been wearing your retainers as directed.

If you’re intrigued by the idea of completing treatment quickly and affordably, you can learn more in our full review of Byte.

Candid vs. SnapCorrect

Since hitting the market in 2017, we think Candid has continuously gone the extra mile to deliver a high-quality patient experience. They started as a fully-remote clear aligner service, but have recently shifted to a hybrid treatment option called “CandidPro” that combines elements of in-office and at-home care.

After an initial in-person consultation and examination with a local dentist, you’ll check in virtually via their CandidMonitoring service every 14 days for the rest of your treatment. By keeping a local dentist involved for the entire treatment process, we think Candid offers a level of personalized care that sets them apart from SnapCorrect, or any other fully remote clear aligner service. During SnapCorrect treatment, you aren’t required to complete any photo check-ins.

Additionally, Candid’s treatment plans can move all your teeth (including molars), laying the groundwork to move your front six teeth without negatively impacting your bite. SnapCorrect treatment focuses primarily on moving your front six teeth.

That said, these premium perks come at a price. Candid treatment starts at $3,500, twice as much as SnapCorrect.

Interested in Candid? Visit our full review to learn more.

SmileDirectClub vs. SnapCorrect

Established in 2014, SmileDirectClub stands out as the largest and most established at-home clear aligner brand. They’ve treated more than two million patients, giving them a long track record of success, and over the years, we think they’ve developed the most convenient treatment out there.

In our opinion, SmileDirectClub makes getting started with treatment incredibly easy. They have more than 100 retail locations and 1,000 partnering dental offices where you can get started with a teeth scan instead of completing an at-home impression kit.

Like Byte, SmileDirectClub offers a nighttime-only treatment option, where you only need to wear your aligners for ten hours per day (while you sleep), rather than the 22+ hours that SnapCorrect requires.

Even though SmileDirectClub has received some complaints about their customer support in the past, it appears that they’ve righted the ship in recent years. They’ve introduced a mobile app that gives you access to their care team seven days a week and a Lifetime Smile Guarantee that provides refinements if your teeth ever shift down the road (assuming that you’ve been wearing your retainers as directed).

For a deep dive into SmileDirectClub treatment, see our full review.

Summary

SnapCorrect certainly isn’t a bad option, especially considering their relatively low price point. However, they don’t do much else to set themselves apart from the crowd. If you’re looking for the best overall value clear aligner option, we recommend Byte.

Frequently Asked Questions

Can SnapCorrect correct my condition?

It depends. SnapCorrect treats mild and moderate cases of crowding and spacing, but it might not be able to correct jaw misalignments like overbite, underbite, crossbite, etc. The only way to know for sure is to complete an impression kit. SnapCorrect’s dental team will analyze your condition and determine whether they can correct it.

What about Invisalign?

The clear aligner innovator has its own set of unique benefits, most notably in-person care. During regular face-to-face checkups, your dentist or orthodontist can make adjustments to your treatment and add attachments that allow Invisalign to treat a wider scope of cases. SnapCorrect is faster and less expensive, but Invisalign is a great option if your condition is severe or you’d prefer to meet with your dentist in person. Our Invisalign review has a ton more information if you’re interested.

How much will I end up paying?

SnapCorrect’s $1,749 sticker price is one of the most attractive in the industry. That said, there are a variety of factors that can influence the price, including sales, financing, insurance, extras, and more. So, at the end of the day, you likely won’t pay that exact amount (although it’ll probably be pretty close). For help estimating what you’ll actually pay, read over our true cost of SnapCorrect guide.

How do I get started?

Before anything else, SnapCorrect’s dental team needs to look at images of your teeth. This means purchasing, completing, and returning an impression kit. Once they have a chance to study your smile, SnapCorrect will develop a digital treatment plan so you can preview every step of your progress.

How long will it take?

According to SnapCorrect’s website, your treatment will probably take between three and nine months, but especially complex cases can last up to 18. Why such a wide range? Because it depends on the complexity of your misalignment. More severe cases simply take longer to correct. After SnapCorrect has had a chance to analyze your teeth, they can estimate how long your treatment will take.

Does insurance cover SnapCorrect’s treatment?

Potentially, but it depends on your provider. The issue is that some insurance companies consider home aligners a cosmetic treatment, so they won’t cover it. However, if your plan includes orthodontic benefits, you may very well receive partial coverage. In this case, you would need to submit a request for reimbursement.

What is the cheapest home aligner service?

Home aligner companies have drastically reduced the cost of teeth-straightening service, but that doesn’t mean they fit perfectly in every budget. If you’re a cost-conscious shopper, check out AlignerCo. Their sticker price is only $995, making them the most affordable service out there (by far). Our full AlignerCo review has more info and you can find other budget-friendly options in our guide on the three most affordable home aligner companies.

Do clear aligners hurt?

When you switch to a new aligner set every two weeks, you might experience some discomfort for the first day or two, but after that, you’ll hardly notice them.

Is home aligner treatment safe?

At-home clear aligner treatment plans are always designed and/or approved by a licensed dentist or orthodontist — as long as you’re buying from a legitimate clear aligner service.

The main concern regarding the safety of fully-remote clear aligner treatment is the lack of face-to-face care. Since you won’t be seeing a dentist in-person during treatment, you won’t receive the same level of support that you’d get with traditional in-office aligners like Invisalign or ClearCorrect. That said, a recent NIH-funded survey found the majority of at-home aligner customers were satisfied with their results, and only 6.6% experienced side effects necessitating a visit to their local dentist.

Read our guide to safe home teeth straightening treatment for more information.

Join The Discussion: